Can A 17-year-old Get Car Insurance In Their Name? Absolutely! At CARS.EDU.VN, we understand the unique challenges young drivers face when trying to secure affordable and reliable car insurance. This guide will provide essential information, expert advice, and practical tips to help 17-year-olds navigate the world of auto insurance. From understanding policy options to finding valuable discounts, CARS.EDU.VN is here to steer you toward the best coverage. Learn about teen driver insurance, new driver policies, and affordable coverage solutions.

1. Understanding Car Insurance for 17-Year-Olds

Navigating the world of car insurance can be daunting, especially for new drivers. It’s important to understand the basics of coverage, costs, and legal requirements. Being informed empowers you to make the best decisions for your specific situation. Let’s explore what you need to know.

1.1. The Legal Landscape

Most states require drivers to have car insurance to legally operate a vehicle. The specific requirements vary by state, but generally include liability coverage, which protects you if you cause an accident and injure someone or damage their property. Some states also require uninsured/underinsured motorist coverage, which protects you if you are hit by a driver without insurance or with insufficient coverage.

1.2. Why Insurance Rates are Higher for Young Drivers

Insurance companies assess risk based on various factors, and age is a significant one. 17-year-olds are statistically more likely to be involved in accidents due to their lack of experience and higher propensity for risky behavior behind the wheel. This higher risk translates to higher insurance premiums.

1.3. Key Factors Influencing Insurance Rates

Several factors influence how much you’ll pay for car insurance. These include:

- Age: Younger drivers typically pay more.

- Driving Record: A clean record means lower rates. Accidents and tickets increase premiums.

- Type of Car: Sports cars and expensive vehicles cost more to insure.

- Location: Urban areas with higher accident rates often have higher premiums.

- Coverage Level: More comprehensive coverage means higher costs.

- Credit Score: In some states, a lower credit score can increase your insurance rates.

1.4. Types of Car Insurance Coverage

Understanding the different types of coverage is crucial for making informed decisions. Here’s a breakdown:

- Liability Coverage: Covers damages and injuries you cause to others. It’s usually required by law.

- Collision Coverage: Pays for damage to your car if you’re in an accident, regardless of fault.

- Comprehensive Coverage: Covers damage to your car from non-accident events like theft, vandalism, or natural disasters.

- Uninsured/Underinsured Motorist Coverage: Protects you if you’re hit by a driver without insurance or with insufficient coverage.

- Personal Injury Protection (PIP): Covers medical expenses for you and your passengers, regardless of fault (required in some states).

2. Can a 17-Year-Old Obtain Car Insurance in Their Own Name?

The short answer is yes, but there are typically some stipulations. Here’s a more detailed explanation.

2.1. Co-signing and Legal Requirements

In most states, a 17-year-old can purchase car insurance in their name. However, because 17-year-olds are considered minors, they usually need a parent or guardian to co-sign the policy. This ensures that there is a legally responsible adult attached to the contract. Co-signing means the parent or guardian is equally responsible for the policy and any associated liabilities.

2.2. Emancipated Minors

An exception to the co-signing rule is if the 17-year-old is an emancipated minor. Emancipation is a legal process where a minor is granted the rights of an adult, including the ability to enter into contracts. If a 17-year-old is legally emancipated, they can purchase car insurance without a co-signer.

2.3. Registering the Vehicle

To get car insurance in your name, you typically need to be the registered owner of the vehicle. This means the title of the car must be in your name. If the car is registered to someone else, they will need to be the primary policyholder.

3. Exploring Insurance Options: Individual Policy vs. Family Policy

When it comes to insuring a 17-year-old driver, you have two main options: an individual policy or adding the teen to the family’s existing policy. Each option has its own advantages and disadvantages.

3.1. Individual Car Insurance Policy

An individual policy is a separate insurance policy specifically for the 17-year-old driver.

Pros:

- Build Credit: Making timely payments on an individual policy can help a young driver build their credit history.

- Independence: An individual policy gives the teen driver a sense of independence and responsibility.

- Customized Coverage: You can tailor the coverage to the teen’s specific needs and driving habits.

Cons:

- Higher Cost: Individual policies for young drivers are typically much more expensive than adding them to a family policy.

- Limited Discounts: Young drivers may not be eligible for as many discounts on an individual policy.

3.2. Adding a Teen to a Family Policy

Adding a 17-year-old to an existing family car insurance policy is a common and often more affordable option.

Pros:

- Lower Cost: Adding a teen to a family policy is generally less expensive than purchasing an individual policy.

- Discounts: You may be eligible for multi-car discounts and other family-related discounts.

- Convenience: Managing one policy for the entire family is often more convenient.

Cons:

- Increased Premiums: Adding a teen driver will likely increase your overall premium, even with discounts.

- Impact on Family Rates: If the teen driver is involved in an accident, it could raise the rates for the entire family.

3.3. Comparing Costs and Coverage

To make the best decision, it’s important to compare the costs and coverage options of both individual policies and adding the teen to a family policy. Get quotes from multiple insurance companies to see which option offers the best value.

3.4. Case Study: Real-World Examples

Consider two scenarios:

- Scenario 1: The Smith family has two cars and a clean driving record. Adding their 17-year-old son to their policy increases their premium by $1,200 per year. An individual policy for their son costs $3,000 per year.

- Scenario 2: The Jones family has one car and a less-than-perfect driving record. Adding their 17-year-old daughter to their policy increases their premium by $1,800 per year. An individual policy for their daughter costs $2,500 per year.

In the first scenario, adding the teen to the family policy is the more cost-effective option. In the second scenario, an individual policy might be a better choice.

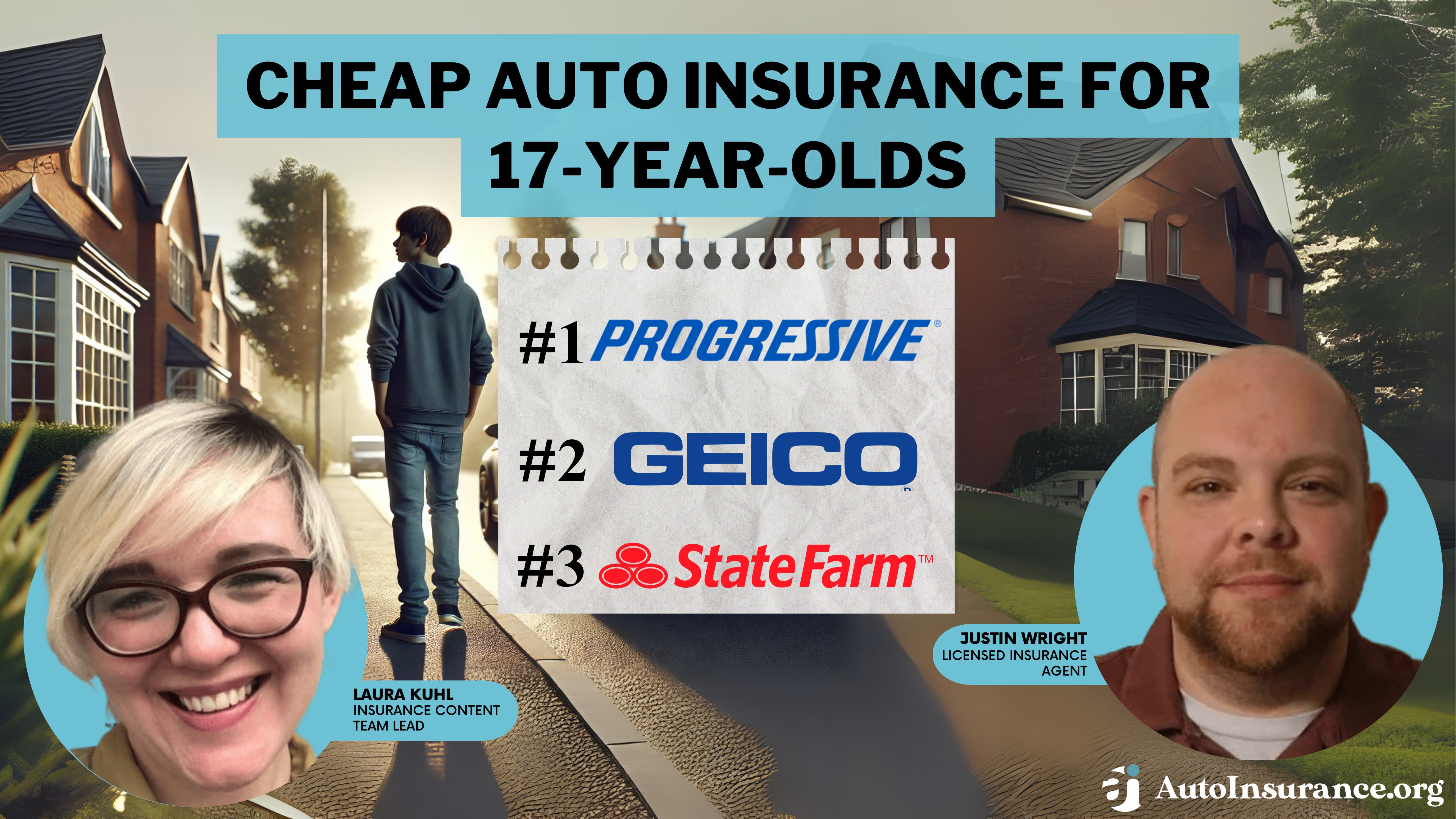

4. Top Car Insurance Companies for 17-Year-Olds

Choosing the right insurance company can make a big difference in both cost and coverage. Here are some of the top companies that offer competitive rates and comprehensive coverage for young drivers.

4.1. Progressive

Progressive is often cited as one of the cheapest options for 17-year-olds.

Pros:

- Affordable Rates: Progressive generally offers competitive rates for young drivers.

- Snapshot Program: This usage-based program allows safe drivers to earn discounts by tracking their driving habits.

Cons:

- Customer Service: Some customers report mixed experiences with Progressive’s customer service.

- Rate Fluctuations: Rates can vary significantly based on driving record and location.

4.2. Geico

Geico is another popular choice for teen drivers, known for its discounts and user-friendly app.

Pros:

- Competitive Rates: Geico offers affordable rates for many drivers, including teens.

- Discounts: Geico offers a variety of discounts for students, safe drivers, and more.

- Mobile App: The Geico app makes it easy to manage your policy and file claims.

Cons:

- Customer Service: Customer service reviews can be mixed.

- Limited Coverage Options: Geico doesn’t offer as many add-on coverage options as some other companies.

4.3. State Farm

State Farm is known for its strong financial stability and extensive network of local agents.

Pros:

- Local Agents: State Farm’s local agents provide personalized service and support.

- Good Student Discount: State Farm offers a significant discount for students with good grades.

- Financial Stability: State Farm is a financially strong company with a reputation for paying claims promptly.

Cons:

- Higher Rates: State Farm’s rates can be higher than some competitors, especially for high-risk drivers.

- Limited Digital Tools: State Farm’s digital tools aren’t as advanced as some other companies.

4.4. Allstate

Allstate offers a variety of coverage options and discounts, including a usage-based program called Drivewise.

Pros:

- Drivewise Program: This program rewards safe driving habits with discounts.

- Coverage Options: Allstate offers a wide range of coverage options to customize your policy.

- Financial Stability: Allstate is a financially stable company.

Cons:

- Higher Rates: Allstate’s rates can be higher than some competitors.

- Customer Service: Customer service reviews are mixed.

4.5. Other Companies to Consider

- Farmers: Known for customizable policies and good student discounts.

- Nationwide: Offers vanishing deductibles and multiple coverage options.

- Liberty Mutual: Provides usage-based discounts and a good student discount.

- Esurance: Offers online convenience and an easy claims process.

- Travelers: Known for strong financial stability and roadside assistance.

5. Understanding Auto Insurance Rates for 17-Year-Old Drivers

Auto insurance rates for 17-year-old drivers are generally higher than those for older, more experienced drivers. This is due to a variety of factors. Understanding these factors can help you make informed decisions about your coverage and potentially lower your costs.

5.1. Factors Affecting Insurance Costs

Several key factors influence the cost of auto insurance for 17-year-old drivers:

- Age and Experience: Younger drivers have less experience behind the wheel, making them statistically more likely to be involved in accidents.

- Driving Record: A clean driving record will result in lower rates. Accidents, tickets, and other violations will increase premiums.

- Type of Vehicle: The make and model of the vehicle can significantly impact insurance rates. Sports cars and other high-performance vehicles are typically more expensive to insure.

- Coverage Level: The amount of coverage you choose will affect your rates. Higher liability limits, collision coverage, and comprehensive coverage will all increase your premium.

- Location: Insurance rates vary by state and even by ZIP code. Urban areas with higher accident rates generally have higher premiums.

- Credit Score: In some states, insurance companies use credit scores to determine rates. A lower credit score can result in higher premiums.

- Discounts: Various discounts are available, such as good student discounts, driver education discounts, and multi-policy discounts.

5.2. Average Insurance Costs for 17-Year-Olds

The average cost of auto insurance for a 17-year-old driver can range from $150 to $400 per month for full coverage. However, this is just an estimate, and the actual cost will vary depending on the factors mentioned above.

- State Averages: Some states have higher average insurance rates than others. For example, states with high population density and frequent accidents tend to have higher rates.

- Urban vs. Rural: Urban areas typically have higher rates due to increased traffic and a higher risk of accidents and theft.

- Gender: Statistically, young male drivers tend to pay more for insurance than young female drivers due to higher accident rates.

5.3. Impact of Driving Record on Insurance Rates

A clean driving record is crucial for keeping insurance rates low. Even a single ticket or accident can significantly increase your premium.

- Speeding Tickets: A speeding ticket can increase your insurance rate by 10% to 20% or more.

- Accidents: Being involved in an accident, even if you’re not at fault, can raise your rates. At-fault accidents will have a more significant impact.

- DUIs: Driving under the influence (DUI) is a serious offense that will result in a substantial increase in your insurance rates. It may also lead to policy cancellation.

5.4. Sample Rate Comparisons

Here are some sample rate comparisons for a 17-year-old driver with a clean driving record, driving a moderate-risk vehicle, and living in an average-cost state:

| Insurance Company | Monthly Premium | Annual Premium |

|---|---|---|

| Progressive | $250 | $3,000 |

| Geico | $275 | $3,300 |

| State Farm | $300 | $3,600 |

| Allstate | $325 | $3,900 |

5.5. Tips for Lowering Insurance Costs

Several strategies can help 17-year-old drivers lower their auto insurance costs:

- Maintain a Clean Driving Record: Drive safely and avoid tickets and accidents.

- Take a Driver Education Course: Many insurance companies offer discounts for completing a driver education course.

- Get Good Grades: Most insurers provide a good student discount for maintaining a B average or higher.

- Choose a Safe Vehicle: Insure a vehicle with good safety ratings and lower repair costs.

- Increase Your Deductible: A higher deductible will lower your premium, but you’ll need to pay more out-of-pocket in the event of a claim.

- Shop Around: Get quotes from multiple insurance companies to compare rates and coverage.

- Consider Usage-Based Insurance: Programs like Progressive’s Snapshot and Allstate’s Drivewise track your driving habits and reward safe drivers with discounts.

- Bundle Policies: If your family has other insurance policies, such as homeowners insurance, consider bundling them with your auto insurance for a multi-policy discount.

Teenage Driver Car Insurance

Teenage Driver Car Insurance

6. Discounts Available for 17-Year-Old Drivers

One of the best ways to reduce car insurance costs is by taking advantage of available discounts. Here are some common discounts for 17-year-old drivers.

6.1. Good Student Discount

Many insurance companies offer a discount to students who maintain a B average or higher. This is because studies show that good students tend to be more responsible and less likely to be involved in accidents.

- Eligibility Requirements: Typically, you’ll need to provide proof of your grades, such as a report card or transcript.

- Discount Amount: The discount amount varies by company but can range from 10% to 25% or more.

6.2. Driver Education Discount

Completing a driver education course can also qualify you for a discount. These courses teach safe driving techniques and help new drivers develop good habits.

- Approved Courses: Make sure the course is approved by your insurance company to be eligible for the discount.

- Discount Amount: The discount amount varies but is typically around 5% to 10%.

6.3. Multi-Policy Discount

If your family has other insurance policies with the same company, such as homeowners insurance or renters insurance, you may be eligible for a multi-policy discount.

- Bundling: Bundling multiple policies can save you a significant amount of money on your overall insurance costs.

- Discount Amount: The discount amount varies but can range from 5% to 15% or more.

6.4. Multi-Car Discount

If your family insures multiple cars with the same company, you may be eligible for a multi-car discount.

- Eligibility: To qualify, all vehicles must be registered to the same address.

- Discount Amount: The discount amount varies but can range from 5% to 20% or more.

6.5. Usage-Based Insurance Discounts

Usage-based insurance programs track your driving habits and reward safe drivers with discounts.

- How it Works: These programs use a mobile app or device installed in your car to monitor your driving behavior.

- Factors Tracked: Common factors tracked include speed, braking, mileage, and time of day.

- Potential Savings: Safe drivers can save up to 30% or more on their insurance premiums.

6.6. Other Potential Discounts

- Defensive Driving Course: Taking a defensive driving course can qualify you for a discount.

- Anti-Theft Device Discount: Installing an anti-theft device in your car can lower your comprehensive coverage costs.

- Good Paving Discount: Some insurance companies offer discounts for students who live more than 100 miles away from home and only drive their car occasionally.

6.7. How to Inquire About and Apply for Discounts

- Ask Your Insurance Agent: Ask your insurance agent about all available discounts and how to qualify.

- Review Your Policy: Review your policy documents to see if you’re already receiving any discounts.

- Provide Documentation: Be prepared to provide documentation to verify your eligibility for discounts, such as a report card or certificate of completion for a driver education course.

7. Factors That Can Increase Insurance Premiums

While discounts can help lower your insurance costs, certain factors can increase your premiums. Here are some of the most common factors that can lead to higher insurance rates for 17-year-old drivers.

7.1. Accidents and Traffic Violations

Accidents and traffic violations are two of the biggest factors that can increase your insurance premiums. Even a minor fender-bender or a single speeding ticket can have a significant impact on your rates.

- At-Fault Accidents: If you’re found to be at fault in an accident, your insurance rates will likely increase substantially.

- Traffic Tickets: Speeding tickets, red light violations, and other traffic tickets can also raise your rates.

- Severity Matters: The more serious the accident or violation, the greater the impact on your insurance premiums.

7.2. Type of Vehicle

The type of vehicle you drive can also affect your insurance rates. Sports cars and other high-performance vehicles are typically more expensive to insure than sedans or SUVs.

- Risk Factors: Insurance companies consider factors such as the vehicle’s horsepower, safety features, and repair costs when determining rates.

- High-Risk Vehicles: Vehicles with a high risk of theft or damage are also more expensive to insure.

7.3. Location

Your location can also play a role in determining your insurance rates. Drivers who live in urban areas with high traffic density and a high risk of accidents and theft typically pay more for insurance than those who live in rural areas.

- City vs. Rural: Urban areas have higher rates due to increased traffic and a greater risk of accidents and theft.

- State Variations: Some states have higher average insurance rates than others due to factors such as weather conditions and legal requirements.

7.4. Coverage Levels

The amount of coverage you choose can also affect your insurance rates. Higher liability limits, collision coverage, and comprehensive coverage will all increase your premium.

- Balancing Cost and Coverage: It’s important to strike a balance between cost and coverage to ensure you have adequate protection without paying more than you need to.

- Consider Your Needs: Consider your individual needs and risk tolerance when choosing coverage levels.

7.5. Credit Score (in Some States)

In some states, insurance companies use credit scores to determine rates. Drivers with lower credit scores typically pay more for insurance than those with higher credit scores.

- Credit-Based Insurance Scores: These scores are based on your credit history and are used to assess your risk as a driver.

- State Regulations: Not all states allow insurance companies to use credit scores to determine rates.

7.6. Other Factors

- Driving Experience: Drivers with less experience typically pay more for insurance.

- Gender: In some cases, young male drivers may pay more for insurance than young female drivers due to statistical differences in accident rates.

7.7. Steps to Take if Your Rates Increase

If your insurance rates increase, there are several steps you can take to try to lower them:

- Shop Around: Get quotes from multiple insurance companies to compare rates and coverage.

- Increase Your Deductible: A higher deductible will lower your premium, but you’ll need to pay more out-of-pocket in the event of a claim.

- Review Your Coverage: Make sure you have the right amount of coverage for your needs.

- Ask About Discounts: Inquire about any available discounts that you may be eligible for.

- Improve Your Driving Record: Drive safely and avoid tickets and accidents.

- Improve Your Credit Score: If you live in a state where credit scores are used to determine insurance rates, take steps to improve your credit score.

8. Tips for Finding Affordable Car Insurance

Finding affordable car insurance as a 17-year-old can be a challenge, but it’s definitely possible. Here are some practical tips to help you find the best rates and coverage.

8.1. Shop Around and Compare Quotes

The most important thing you can do is shop around and compare quotes from multiple insurance companies. Don’t just settle for the first quote you receive.

- Online Comparison Tools: Use online comparison tools to get quotes from multiple companies at once.

- Independent Agents: Consider working with an independent insurance agent who can compare quotes from multiple companies on your behalf.

- Direct Quotes: Get quotes directly from insurance companies’ websites or by calling their customer service departments.

8.2. Increase Your Deductible

Increasing your deductible can lower your insurance premium. A deductible is the amount you pay out-of-pocket before your insurance coverage kicks in.

- Higher Deductible, Lower Premium: A higher deductible means you’ll pay more out-of-pocket in the event of a claim, but it will lower your monthly premium.

- Consider Your Budget: Choose a deductible that you can afford to pay if you need to file a claim.

8.3. Choose the Right Car

The type of car you drive can significantly impact your insurance rates. Choose a car that is safe, reliable, and affordable to insure.

- Safety Ratings: Look for cars with good safety ratings from organizations like the Insurance Institute for Highway Safety (IIHS) and the National Highway Traffic Safety Administration (NHTSA).

- Low-Risk Vehicles: Avoid sports cars and other high-performance vehicles, as they are typically more expensive to insure.

- Affordable Repair Costs: Choose a car with affordable repair costs to keep your insurance rates down.

8.4. Take Advantage of Discounts

Take advantage of all available discounts to lower your insurance costs.

- Good Student Discount: Maintain a B average or higher to qualify for a good student discount.

- Driver Education Discount: Complete a driver education course to qualify for a driver education discount.

- Multi-Policy Discount: Bundle your auto insurance with other policies, such as homeowners insurance, to qualify for a multi-policy discount.

- Usage-Based Insurance: Participate in a usage-based insurance program to earn discounts for safe driving habits.

8.5. Improve Your Driving Habits

Improving your driving habits can help you avoid accidents and traffic tickets, which can lead to lower insurance rates.

- Drive Safely: Follow traffic laws, avoid speeding, and be aware of your surroundings.

- Avoid Distractions: Put away your phone and avoid other distractions while driving.

- Maintain Your Vehicle: Keep your car in good condition to avoid accidents caused by mechanical failure.

8.6. Consider Usage-Based Insurance

Usage-based insurance (UBI) programs track your driving habits and reward safe drivers with discounts.

- How it Works: UBI programs use a mobile app or device installed in your car to monitor your driving behavior.

- Potential Savings: Safe drivers can save up to 30% or more on their insurance premiums.

8.7. Shop Around Regularly

Insurance rates can change over time, so it’s a good idea to shop around and compare quotes regularly.

- Annual Review: Review your insurance policy annually to make sure you’re still getting the best rates and coverage.

- Life Changes: Update your insurance policy whenever you experience a major life change, such as moving to a new address or buying a new car.

8.8. Consult with an Insurance Professional

If you’re feeling overwhelmed or unsure about your insurance options, consider consulting with an insurance professional.

- Independent Agents: Independent agents can provide personalized advice and compare quotes from multiple companies on your behalf.

- Company Representatives: Company representatives can answer your questions and help you choose the right coverage for your needs.

9. Common Mistakes to Avoid

When it comes to car insurance, it’s easy to make mistakes that can cost you money or leave you without adequate coverage. Here are some common mistakes to avoid.

9.1. Not Shopping Around

One of the biggest mistakes you can make is not shopping around and comparing quotes from multiple insurance companies.

- Settle for the First Quote: Don’t just settle for the first quote you receive.

- Compare Rates and Coverage: Compare rates and coverage options from multiple companies to find the best deal.

9.2. Choosing the Wrong Coverage Levels

Choosing the wrong coverage levels can leave you without adequate protection in the event of an accident.

- Too Little Coverage: Don’t choose the minimum coverage required by law without considering your individual needs and risk tolerance.

- Too Much Coverage: Don’t pay for coverage you don’t need.

9.3. Not Understanding Your Policy

Not understanding your insurance policy can lead to confusion and frustration when you need to file a claim.

- Read Your Policy Documents: Take the time to read and understand your policy documents.

- Ask Questions: Ask your insurance agent or company representative if you have any questions about your coverage.

9.4. Not Disclosing Accurate Information

Not disclosing accurate information on your insurance application can lead to denial of coverage or cancellation of your policy.

- Be Honest: Be honest about your driving record, vehicle information, and other relevant details.

- Update Information: Update your insurance policy whenever you experience a major life change, such as moving to a new address or buying a new car.

9.5. Ignoring Discounts

Ignoring available discounts can cost you money on your insurance premiums.

- Ask About Discounts: Ask your insurance agent about all available discounts and how to qualify.

- Provide Documentation: Be prepared to provide documentation to verify your eligibility for discounts, such as a report card or certificate of completion for a driver education course.

9.6. Driving Without Insurance

Driving without insurance is illegal and can have serious consequences.

- Financial Penalties: You could face fines, suspension of your driver’s license, and even jail time.

- Liability: If you’re involved in an accident while driving without insurance, you could be held personally liable for damages and injuries.

9.7. Not Filing Claims Properly

Not filing claims properly can lead to delays or denial of coverage.

- Report Accidents Promptly: Report accidents to your insurance company as soon as possible.

- Gather Information: Gather as much information as possible about the accident, including the other driver’s name and insurance information.

- Follow Instructions: Follow your insurance company’s instructions for filing a claim.

9.8. Canceling Your Policy Prematurely

Canceling your insurance policy prematurely can lead to a lapse in coverage, which can increase your rates in the future.

- Avoid Lapses: Avoid allowing your insurance policy to lapse.

- Shop Around First: Shop around and compare quotes before canceling your current policy.

9.9. Neglecting to Review Your Policy Regularly

Neglecting to review your insurance policy regularly can lead to outdated coverage and missed opportunities for savings.

- Annual Review: Review your insurance policy annually to make sure you’re still getting the best rates and coverage.

- Life Changes: Update your insurance policy whenever you experience a major life change, such as moving to a new address or buying a new car.

10. Real-Life Scenarios and Examples

To illustrate the concepts discussed, let’s look at some real-life scenarios and examples.

10.1. Scenario 1: The Good Student

Sarah is a 17-year-old student with a B average. She wants to get her own car insurance policy.

- Challenge: Sarah’s rates are high due to her age and lack of driving experience.

- Solution: Sarah shops around and compares quotes from multiple insurance companies. She also takes advantage of the good student discount, which lowers her premium by 15%.

- Result: Sarah finds an affordable policy with adequate coverage.

10.2. Scenario 2: The New Driver

John is a 17-year-old who just got his driver’s license. He wants to be added to his parents’ insurance policy.

- Challenge: Adding John to his parents’ policy will increase their premium.

- Solution: John’s parents shop around and compare quotes from multiple insurance companies. They also take advantage of the multi-car discount and the safe driver discount.

- Result: John is added to his parents’ policy, and their premium increase is manageable.

10.3. Scenario 3: The Accident

Emily is a 17-year-old who is involved in an accident. She is found to be at fault.

- Challenge: Emily’s insurance rates will likely increase substantially due to the accident.

- Solution: Emily takes a defensive driving course to improve her driving skills and lower her insurance rates. She also works with her insurance company to file a claim properly.

- Result: Emily’s insurance rates increase, but she is able to mitigate the impact by taking a defensive driving course.

10.4. Scenario 4: The Safe Driver

David is a 17-year-old who is a safe driver. He participates in a usage-based insurance program.

- Challenge: David wants to lower his insurance rates.

- Solution: David participates in a usage-based insurance program, which tracks his driving habits. He drives safely and earns a discount of 20% on his insurance premiums.

- Result: David’s insurance rates decrease due to his safe driving habits.

10.5. Scenario 5: The Ticket

Maria is a 17-year-old who receives a speeding ticket.

- Challenge: Maria’s insurance rates will likely increase due to the ticket.

- Solution: Maria attends traffic school to have the ticket removed from her record. She also shops around for better insurance rates.

- Result: Maria is able to minimize the impact of the speeding ticket on her insurance rates.

11. Resources for 17-Year-Old Drivers

Navigating the world of car insurance can be complex, but there are many resources available to help 17-year-old drivers make informed decisions. Here are some helpful resources.

11.1. CARS.EDU.VN

CARS.EDU.VN is a comprehensive resource for all things automotive. You can find articles, guides, and tools to help you understand car insurance, compare rates, and find discounts. We offer expert advice and practical tips to help you navigate the world of car insurance with confidence. At cars.edu.vn, we are committed to providing valuable information and resources to help you make the best decisions for your specific needs.

11.2. Insurance Company Websites

Most insurance companies have websites that provide information about their products and services. You can use these websites to get quotes, compare coverage options, and learn about discounts.

- Progressive: Progressive’s website offers online quotes, policy information, and resources for young drivers.

- Geico: Geico’s website provides online quotes, mobile app access, and information about discounts.

- State Farm: State Farm’s website offers online quotes, local agent information, and resources for students.

- Allstate: Allstate’s website provides online quotes, policy information, and resources for safe drivers.

11.3. State Insurance Departments

State insurance departments regulate the insurance industry and provide consumer protection. You can use these websites to learn about insurance laws and regulations in your state, file complaints, and find consumer resources.

- National Association of Insurance Commissioners (NAIC): The NAIC website provides information about state insurance departments and consumer resources.

11.4. Non-Profit Organizations

Non-profit organizations like the Insurance Information Institute (III) and the National Safety Council (NSC) provide educational resources about car insurance and safe driving.

- Insurance Information Institute (III): The III website offers articles, guides, and tools to help you understand car insurance.

- National Safety Council (NSC): The NSC website provides information about safe driving practices and accident prevention.

11.5. Consumer Advocacy Groups

Consumer advocacy groups like the Consumer Federation of America (CFA) advocate for consumer rights and provide information about insurance and other financial products.

- Consumer Federation of America (CFA): The CFA website offers articles, guides, and tools to help you make informed financial decisions.

11.6. Online Forums and Communities

Online forums and communities can be a valuable source of information and support. You can connect with other drivers, ask questions, and share experiences.

- Reddit: The r/insurance and r/cars subreddits are popular online communities where you can discuss car insurance and other automotive topics.

- Online Forums: Online forums like Car Talk and Edmunds offer discussions about car insurance and other automotive topics.

11.7. Financial Advisors

Financial advisors can provide personalized advice about insurance and other financial products.

- Certified Financial Planner (CFP): A CFP is a financial advisor who has met certain education and experience requirements and has passed a certification exam.

11.8. Insurance Agents and Brokers

Insurance agents and brokers can provide personalized advice and help you find the best insurance rates and coverage.

- Independent Agents: Independent agents work with multiple insurance companies and can compare quotes on your behalf.

- Captive Agents: Captive agents work for a single insurance company and can only offer products from that company.

12. Frequently Asked Questions (FAQs)

Here are some frequently asked questions about car insurance for 17-year-old drivers.

12.1. Can a 17-year-old get their own auto insurance policy?

Yes, in most cases, a 17-year-old can get their own auto insurance policy. However, laws and regulations regarding this matter may vary depending on the state and insurance company. It’s advisable to check with the insurance provider to understand their specific requirements and eligibility criteria.

12.2. How much does auto insurance cost for a 17-year-old?

Auto insurance premiums for 17-year-olds tend to be higher compared to older, more experienced drivers due to their lack of driving experience and higher risk of accidents. The exact cost will depend on various factors such as the 17-year-old’s driving record, location, the type of car they drive, coverage limits, and more. It’s recommended to obtain quotes from different insurance providers to compare rates.