How much is car insurance for an 18-year-old? Understanding car insurance costs for young drivers can be challenging, but CARS.EDU.VN is here to help you navigate the world of auto insurance. We’ll explore the factors that influence these rates and offer practical advice on finding affordable coverage options. Discover the ins and outs of teen driver insurance, young driver car insurance, and strategies for minimizing expenses.

1. Understanding Car Insurance Costs for 18-Year-Olds

It’s no secret that insuring an 18-year-old driver can significantly impact your wallet. Young drivers, statistically, are more prone to accidents due to their inexperience. This higher risk translates to increased insurance premiums. According to the Insurance Institute for Highway Safety (IIHS), the fatal crash rate per mile driven is nearly three times higher for drivers aged 16-19 compared to those 20 and older. Therefore, car insurance companies adjust their rates to reflect this elevated risk.

1.1. Average Costs: Adding to a Parent’s Policy vs. Standalone Coverage

One of the first decisions you’ll face is whether to add your 18-year-old to your existing policy or allow them to purchase their own. Generally, adding a teen to a parent’s policy is more cost-effective. Forbes Advisor’s analysis indicates that the average yearly cost to add an 18-year-old to a parent’s car insurance policy is $2,103, or about $175 per month.

However, if an 18-year-old opts for their own policy, the average cost skyrockets to $6,147 per year, or roughly $512 each month. This significant difference underscores the financial advantage of family policies. Remember, these are averages, and your actual costs may vary based on your specific circumstances.

Cost Comparison

| Policy Type | Average Annual Cost | Average Monthly Cost |

|---|---|---|

| Added to Parent’s Policy | $2,103 | $175 |

| Standalone Policy (18-year-old) | $6,147 | $512 |

1.2. Factors Influencing Car Insurance Rates for Young Adults

Several factors influence car insurance costs for 18-year-olds. Understanding these can help you anticipate and potentially mitigate expenses.

- Age and Experience: Younger drivers inherently lack driving experience, which insurance companies view as a higher risk.

- Gender: Statistically, young male drivers are involved in more accidents than their female counterparts. Consequently, insurance rates for young males tend to be higher.

- Location: Urban areas with high traffic density often have higher insurance rates than rural areas. Factors such as accident frequency, theft rates, and repair costs in your location play a role.

- Type of Vehicle: The make and model of the car significantly impact insurance costs. Sports cars or expensive vehicles typically have higher premiums due to their increased repair or replacement costs.

- Driving Record: Any history of accidents or traffic violations will lead to higher insurance rates. Maintaining a clean driving record is crucial for affordability.

- Coverage Levels: The amount of coverage you choose also influences costs. Higher liability limits, comprehensive, and collision coverage will increase premiums.

1.3. CARS.EDU.VN: Your Resource for Affordable Car Insurance

At CARS.EDU.VN, we understand the challenges of finding affordable car insurance for young drivers. Our platform offers resources, tips, and expert advice to help you make informed decisions. We provide insights into various insurance providers, coverage options, and strategies for lowering costs.

2. Comparing Car Insurance Companies for 18-Year-Olds

Shopping around is essential to securing the most favorable rates. Different insurance companies use varying formulas to calculate premiums, so the costs can differ significantly. Forbes Advisor’s research highlights some companies that offer more competitive rates for young drivers.

2.1. Cheapest Options for Adding an 18-Year-Old to a Parent’s Policy

According to Forbes Advisor, USAA generally offers the cheapest rates for adding an 18-year-old to a parent’s policy, but it’s exclusively available to military members, veterans, and their families. Other affordable alternatives include Erie and Geico. Erie’s cost to add a driver age 18 is approximately $634 per year less than the average, while Geico’s is roughly $564 less.

Cheapest Companies to Add an 18-Year-Old

| Insurance Company | Average Annual Cost to Add 18-Year-Old |

|---|---|

| USAA | $1,153 |

| Erie | $1,469 |

| Geico | $1,539 |

2.2. Affordable Options for Parents Including an 18-Year-Old

When considering the overall cost of a family policy that includes parents and an 18-year-old, USAA, Erie, and Geico remain competitive choices. Travelers and State Farm are also worth considering.

Cheapest Companies for Family Policies with an 18-Year-Old

| Insurance Company | Average Annual Cost for Family Policy |

|---|---|

| USAA | $3,294 |

| Erie | $3,933 |

| Geico | $4,058 |

2.3. Budget-Friendly Choices for Standalone Policies

If an 18-year-old needs their own car insurance policy, it’s especially critical to shop around. USAA, Auto-Owners, and Geico are often cited as more affordable options for standalone policies.

Cheapest Companies for Standalone Policies (18-Year-Old)

| Insurance Company | Average Annual Cost for Standalone Policy |

|---|---|

| USAA | $3,665 |

| Auto-Owners | $4,427 |

| Geico | $4,438 |

2.4. Utilizing CARS.EDU.VN to Compare and Contrast

CARS.EDU.VN simplifies the comparison process by providing tools and resources to evaluate different insurance companies. Our website helps you assess coverage options, read reviews, and obtain quotes, ensuring you find the best fit for your needs and budget.

3. Strategies for Lowering Car Insurance Rates for 18-Year-Olds

While insurance rates for young drivers are typically high, several strategies can help minimize these costs.

3.1. Safe Driving Habits

Encouraging safe driving habits is paramount. A clean driving record is one of the most effective ways to lower insurance rates. This includes avoiding speeding tickets, accidents, and other traffic violations. Consider installing a telematics device that monitors driving behavior and rewards safe driving with lower rates.

3.2. Driver’s Education and Defensive Driving Courses

Completing a driver’s education course or a defensive driving course can sometimes qualify you for a discount. Many insurance companies offer discounts to young drivers who have completed these courses, as they demonstrate a commitment to safe driving.

3.3. Good Student Discount

Many insurers provide a “good student discount” to young drivers who maintain a high GPA or rank in the top percentage of their class. To qualify, students usually need to be enrolled full-time in high school or college and maintain a B average or better.

3.4. Student Away From Home Discount

If an 18-year-old is attending college more than 100 miles away from home and does not regularly drive the vehicle, you may be eligible for a “student away from home” discount. This discount acknowledges that the student is not regularly exposed to driving risks.

3.5. Choosing the Right Vehicle

The type of vehicle driven significantly impacts insurance rates. Opting for a safe, reliable car with a good safety rating can help lower premiums. Avoid high-performance sports cars or luxury vehicles, which are more expensive to insure.

3.6. Increasing Deductibles

Choosing a higher deductible can lower your monthly premiums. However, ensure you can afford the deductible amount if you need to file a claim. This strategy involves balancing lower monthly payments with higher out-of-pocket costs in the event of an accident.

3.7. Reviewing Coverage Options

Evaluate your coverage needs carefully. While it’s essential to have adequate protection, you may be able to adjust your coverage levels to reduce costs. For example, if you have an older vehicle, you might consider dropping collision or comprehensive coverage.

3.8. Leveraging CARS.EDU.VN for Personalized Advice

CARS.EDU.VN offers personalized advice tailored to your specific situation. Our resources help you assess your risk profile, explore discount options, and make informed decisions about coverage levels, ensuring you get the best possible rates.

4. State-Specific Car Insurance Costs for 18-Year-Olds

Car insurance rates can vary significantly from state to state due to factors such as local laws, traffic density, and claim frequencies. Understanding these differences can help you anticipate costs based on your location.

4.1. Cost Variations Across States

States with higher population densities and more frequent accidents generally have higher insurance rates. For example, Florida and Louisiana often have some of the highest car insurance costs in the country, while states like Maine and North Carolina tend to be more affordable.

Sample State-Specific Rates

| State | Average Annual Cost to Add 18-Year-Old | Average Annual Cost for Standalone Policy |

|---|---|---|

| California | $2,613 | $5,707 |

| Florida | $3,080 | $8,688 |

| North Carolina | $894 | $2,593 |

4.2. State-Mandated Coverage Requirements

Each state has its own minimum car insurance coverage requirements. These requirements typically include bodily injury liability and property damage liability. Some states also require uninsured motorist coverage or personal injury protection (PIP). Understanding these requirements is crucial to ensure you have adequate coverage.

4.3. Regional Discounts and Incentives

Some states offer specific discounts or incentives to encourage safe driving or reduce insurance costs. For example, some states may offer tax credits for completing approved driver safety courses. Check with your local insurance agent or DMV to learn about available programs.

4.4. CARS.EDU.VN’s State-Specific Guides

CARS.EDU.VN provides state-specific guides that offer detailed information on car insurance requirements, average costs, and available discounts in your region. These guides help you navigate the complexities of local insurance markets and make informed decisions.

5. Gender-Based Car Insurance Rate Differences

Gender is a significant factor in determining car insurance rates for young drivers. Statistically, young male drivers are involved in more accidents than their female counterparts, leading to higher premiums.

5.1. Average Rate Differences by Gender

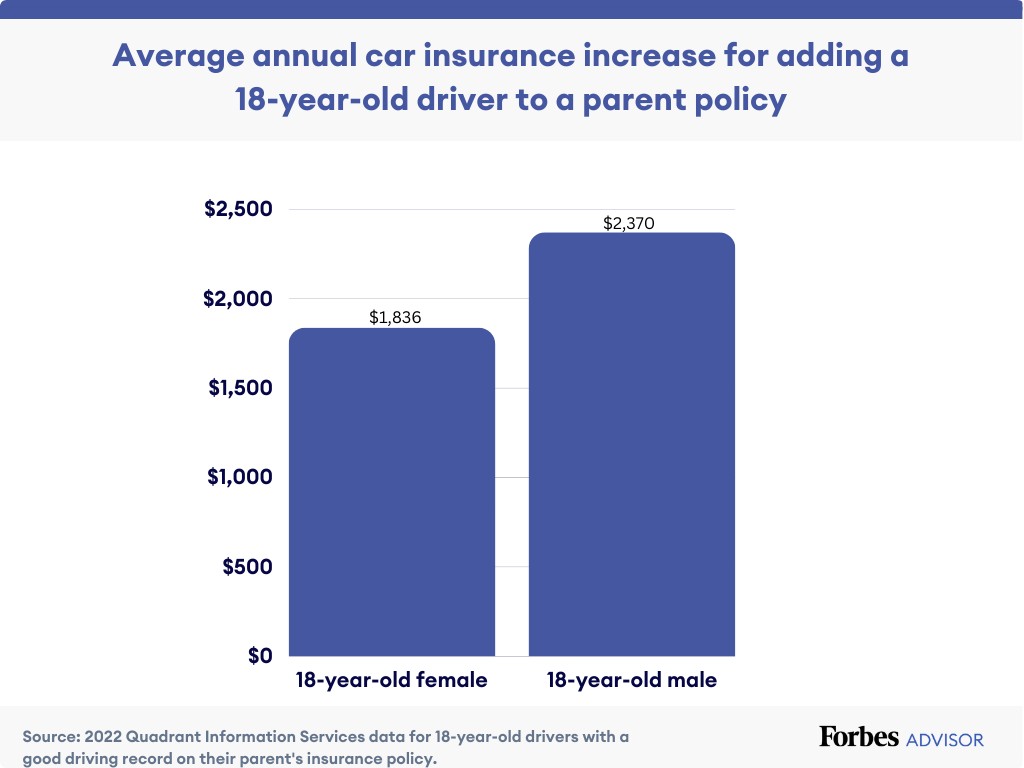

According to Forbes Advisor’s analysis, male 18-year-old drivers pay approximately 29% more for auto insurance than their female counterparts when added to a parent’s policy. The difference is also significant for standalone policies.

Average Rate Differences by Gender

| Policy Type | Average Annual Cost (Female) | Average Annual Cost (Male) | Percentage Increase (Male) |

|---|---|---|---|

| Added to Parent’s Policy | $1,836 | $2,370 | 29% |

| Standalone Policy (18-Year-Old) | $5,656 | $6,638 | 17% |

5.2. Reasons for Gender-Based Disparities

The disparity in rates stems from statistical data indicating that young male drivers are more likely to engage in risky behaviors, such as speeding, drunk driving, and distracted driving, resulting in a higher accident rate.

5.3. Mitigation Strategies for Male Drivers

While male drivers cannot change their gender, they can take steps to mitigate higher insurance rates. Emphasizing safe driving habits, completing defensive driving courses, and maintaining a clean driving record can help lower premiums.

5.4. CARS.EDU.VN’s Insights on Gender-Based Rates

CARS.EDU.VN provides insights and advice on understanding and navigating gender-based insurance rates. Our resources help young male drivers identify strategies to reduce costs and demonstrate responsible driving behavior to insurers.

6. Comparing Coverage Options: Liability, Collision, and Comprehensive

Choosing the right coverage options is essential to protecting yourself financially in the event of an accident. Understanding the different types of coverage and their benefits can help you make informed decisions.

6.1. Liability Coverage

Liability coverage protects you if you are at fault in an accident. It covers the other party’s medical expenses and property damage. Most states have minimum liability coverage requirements, but it’s often wise to purchase higher limits to protect your assets.

6.2. Collision Coverage

Collision coverage pays for damage to your vehicle if you collide with another object, such as a car or a tree. It covers repairs or replacement of your vehicle, regardless of who is at fault.

6.3. Comprehensive Coverage

Comprehensive coverage protects your vehicle from non-collision-related damage, such as theft, vandalism, fire, or natural disasters. It covers repairs or replacement of your vehicle in these situations.

6.4. Uninsured/Underinsured Motorist Coverage

This coverage protects you if you are hit by a driver who has no insurance or insufficient insurance to cover your damages. It covers your medical expenses and vehicle repairs in these situations.

6.5. Personal Injury Protection (PIP)

PIP coverage pays for your medical expenses and lost wages, regardless of who is at fault in an accident. It is required in some states and optional in others.

6.6. Choosing the Right Coverage Levels

The appropriate coverage levels depend on your individual circumstances, including your budget, risk tolerance, and the value of your vehicle. Consult with an insurance agent or use CARS.EDU.VN’s resources to assess your needs and determine the right coverage levels.

7. Common Myths About Car Insurance for Young Drivers

Many misconceptions surround car insurance for young drivers. Debunking these myths can help you make informed decisions and avoid costly mistakes.

7.1. Myth: All Car Insurance Companies Charge the Same Rates

Fact: Car insurance rates can vary significantly between companies. It’s essential to compare quotes from multiple insurers to find the best deal.

7.2. Myth: Red Cars Cost More to Insure

Fact: The color of your car does not affect your insurance rates. Insurers consider factors such as the make, model, and safety features of your vehicle.

7.3. Myth: Older Cars Are Always Cheaper to Insure

Fact: While older cars may have lower liability premiums, they may not have comprehensive or collision coverage. The age and condition of the vehicle, as well as the coverage type, determine the overall cost.

7.4. Myth: Filing a Claim Always Increases Your Rates

Fact: While filing a claim can increase your rates, it depends on the circumstances. Some insurers offer accident forgiveness programs, and not-at-fault accidents may not impact your premiums.

7.5. Myth: Minimum Coverage Is Always Sufficient

Fact: Minimum coverage may not be sufficient to protect your assets in a serious accident. It’s often wise to purchase higher liability limits to ensure adequate protection.

7.6. CARS.EDU.VN’s Myth-Busting Resources

CARS.EDU.VN provides myth-busting resources that address common misconceptions about car insurance. Our articles, guides, and expert advice help you navigate the complexities of the insurance market with confidence.

8. How to Choose the Right Car for an 18-Year-Old to Minimize Insurance Costs

The type of car an 18-year-old drives significantly impacts their insurance costs. Choosing a safe, reliable, and affordable vehicle can help minimize premiums.

8.1. Safety Ratings and Features

Prioritize vehicles with high safety ratings and advanced safety features, such as anti-lock brakes, electronic stability control, and airbags. These features can reduce the risk of accidents and injuries, resulting in lower insurance rates.

8.2. Vehicle Type and Performance

Avoid high-performance sports cars or luxury vehicles, which are more expensive to insure due to their increased repair or replacement costs. Opt for a sedan or small SUV with good fuel efficiency and a reputation for reliability.

8.3. Repair Costs and Availability of Parts

Choose a vehicle with affordable repair costs and readily available parts. Vehicles that are expensive to repair or have scarce parts will have higher insurance premiums.

8.4. Depreciation and Value

Consider the depreciation rate of the vehicle. Vehicles that depreciate quickly may be cheaper to insure, as their replacement value decreases over time.

8.5. Examples of Affordable and Safe Cars for 18-Year-Olds

- Honda Civic: Known for its reliability, safety features, and affordability.

- Toyota Corolla: Another reliable and fuel-efficient option with a good safety record.

- Hyundai Elantra: Offers a good balance of features, safety, and value.

8.6. CARS.EDU.VN’s Vehicle Recommendation Tool

CARS.EDU.VN offers a vehicle recommendation tool that helps you find the best cars for young drivers based on safety ratings, insurance costs, and other factors. Our tool simplifies the decision-making process and ensures you choose a vehicle that meets your needs and budget.

9. Maintaining a Clean Driving Record: Essential for Affordable Insurance

Maintaining a clean driving record is crucial for keeping car insurance rates affordable, especially for young drivers.

9.1. The Impact of Accidents and Traffic Violations

Accidents and traffic violations can significantly increase your insurance premiums. Even minor infractions, such as speeding tickets, can impact your rates.

9.2. Safe Driving Practices

Practice safe driving habits, such as obeying traffic laws, avoiding distractions, and driving defensively. These habits can reduce your risk of accidents and traffic violations.

9.3. Defensive Driving Courses

Consider taking a defensive driving course to improve your driving skills and knowledge. Some insurers offer discounts to drivers who complete these courses.

9.4. Telematics and Safe Driving Programs

Participate in telematics or safe driving programs offered by your insurance company. These programs monitor your driving behavior and reward safe driving with lower rates.

9.5. Monitoring Driving Behavior

Encourage young drivers to monitor their driving behavior and identify areas for improvement. This can help them develop safer driving habits and avoid accidents and traffic violations.

9.6. CARS.EDU.VN’s Safe Driving Resources

CARS.EDU.VN provides safe driving resources that offer tips and advice on improving your driving skills and habits. Our articles, guides, and expert advice help you stay safe on the road and maintain a clean driving record.

10. How CARS.EDU.VN Can Help You Find the Best Car Insurance

At CARS.EDU.VN, we’re dedicated to providing you with the resources, tools, and expert advice you need to find the best car insurance for your needs and budget.

10.1. Comprehensive Car Insurance Guides

Our comprehensive car insurance guides offer detailed information on various topics, including coverage options, discounts, and strategies for lowering costs.

10.2. Insurance Company Reviews and Ratings

We provide reviews and ratings of car insurance companies, helping you assess their reputation, customer service, and claims handling.

10.3. Quote Comparison Tool

Our quote comparison tool allows you to compare quotes from multiple insurance companies, ensuring you find the best rates.

10.4. Expert Advice and Insights

Our team of insurance experts provides advice and insights on various car insurance topics, helping you make informed decisions.

10.5. Personalized Recommendations

We offer personalized recommendations based on your individual circumstances, ensuring you find the best coverage options for your needs.

10.6. Ongoing Support and Resources

We provide ongoing support and resources to help you manage your car insurance policy and stay informed about changes in the insurance market.

Ready to Find Affordable Car Insurance?

Don’t let the high cost of car insurance for 18-year-olds discourage you. Visit CARS.EDU.VN today to explore your options, compare quotes, and find the best coverage at the most affordable price. Our resources can help you navigate the complexities of the insurance market and make informed decisions.

Contact Us:

- Address: 456 Auto Drive, Anytown, CA 90210, United States

- WhatsApp: +1 555-123-4567

- Website: CARS.EDU.VN

Frequently Asked Questions (FAQ)

1. Why is car insurance so expensive for 18-year-olds?

Car insurance is more expensive for 18-year-olds because they are statistically more likely to be involved in accidents due to their inexperience. Insurers view them as high-risk drivers and charge higher premiums to offset this risk.

2. Can you add an 18-year-old to an existing policy?

Yes, you can add an 18-year-old to an existing car insurance policy. In most cases, it is more affordable than having the 18-year-old purchase their own policy.

3. At what age will car insurance rates start to go down?

Car insurance rates typically start to decrease gradually as drivers gain experience. Rates may decrease noticeably around age 21 and continue to decline with age, assuming a clean driving record.

4. Will safe driving influence the cost of car insurance for an 18-year-old driver?

Yes, safe driving habits can positively influence the cost of car insurance for an 18-year-old. Maintaining a clean driving record, avoiding accidents and traffic violations, and participating in safe driving programs can help lower premiums.

5. What is a good student discount, and how can it help lower insurance rates?

A good student discount is a discount offered by insurance companies to young drivers who maintain a high GPA or rank in the top percentage of their class. To qualify, students usually need to be enrolled full-time in high school or college and maintain a B average or better.

6. How does the type of car an 18-year-old drives affect insurance costs?

The type of car an 18-year-old drives can significantly impact insurance costs. High-performance sports cars or luxury vehicles are more expensive to insure due to their increased repair or replacement costs. Opting for a safe, reliable, and affordable vehicle can help minimize premiums.

7. What is the student away from home discount, and who qualifies?

The student away from home discount is a discount offered to young drivers who attend college more than 100 miles away from home and do not regularly drive the insured vehicle. To qualify, the student typically needs to reside at the school and only drive the vehicle during school holiday periods and vacations.

8. Is it better for an 18-year-old to get their own policy or be added to their parent’s policy?

In most cases, it is more affordable for an 18-year-old to be added to their parent’s car insurance policy than to purchase their own policy. Adding a teen to a parent’s policy usually results in significantly lower premiums.

9. What are the key factors that influence car insurance costs for 18-year-olds?

Key factors that influence car insurance costs for 18-year-olds include age, gender, location, type of vehicle, driving record, coverage levels, and available discounts.

10. How can CARS.EDU.VN help me find the best car insurance for an 18-year-old?

cars.edu.vn provides comprehensive car insurance guides, reviews and ratings of insurance companies, a quote comparison tool, expert advice and insights, personalized recommendations, and ongoing support and resources to help you find the best car insurance for an 18-year-old.